MONEX 環球個人投資者調查報告

MONEX 環球個人投資者調查報告

MONEX 環球個人投資者調查報告

2018年06月

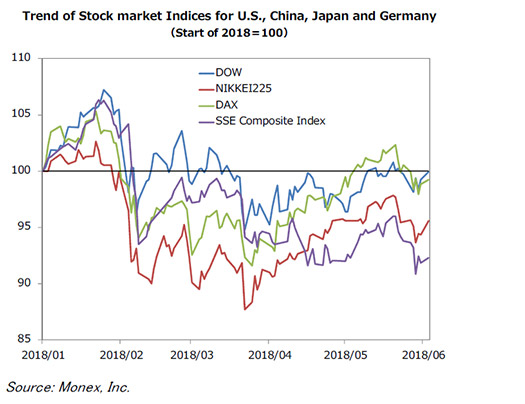

Summary

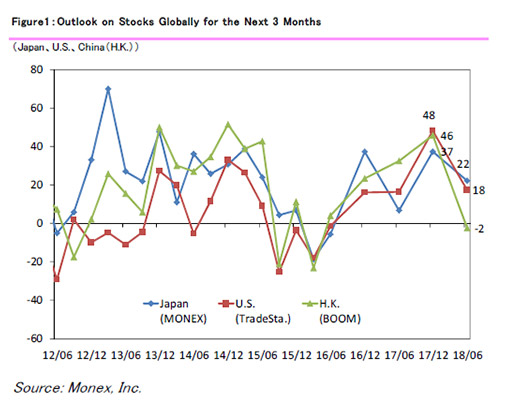

Summary [The forecast DI for world stock markets]

[Japan]

|

Dec. 2017: 37 → June 2018: 22 (-15 points)

|

[U.S.]

|

Dec. 2017: 48 → June 2018: 18 (-30 points)

|

[Forecast DI: China (H.K.)]

|

Dec. 2017: 46 → June 2018: -2 (-48 points)

|

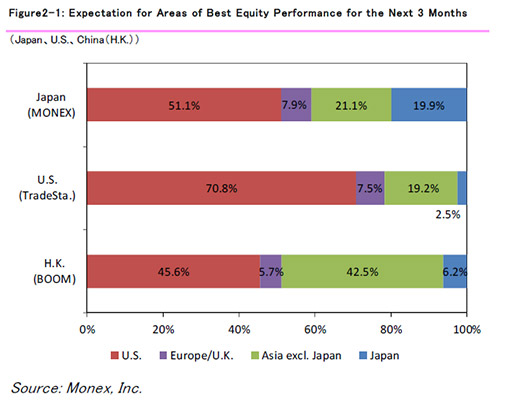

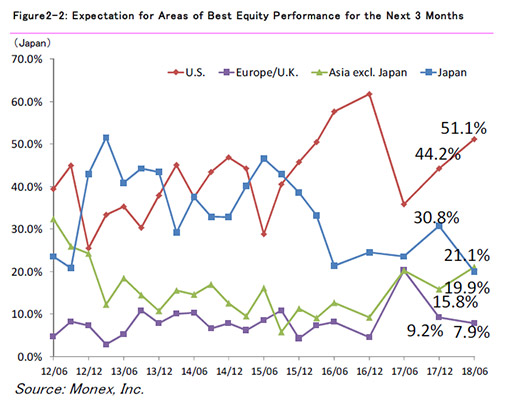

[Expectations for stock markets in the coming three months]

[Japan]

|

U.S.: 51.1%

|

Europe/U.K.: 7.9%

|

Asia excl. Japan: 21.1%

|

Japan: 19.9%

|

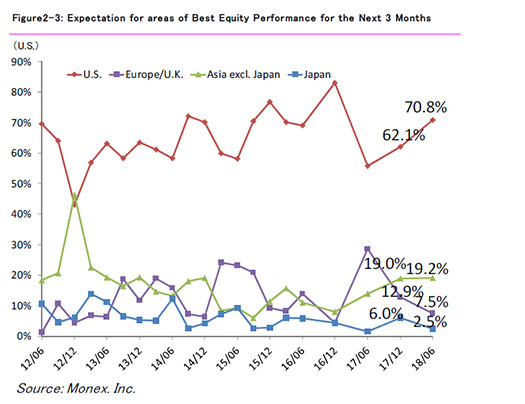

[U.S.]

|

U.S.: 70.8%

|

Europe/U.K.: 7.5%

|

Asia excl. Japan: 19.2%

|

Japan: 2.5%

|

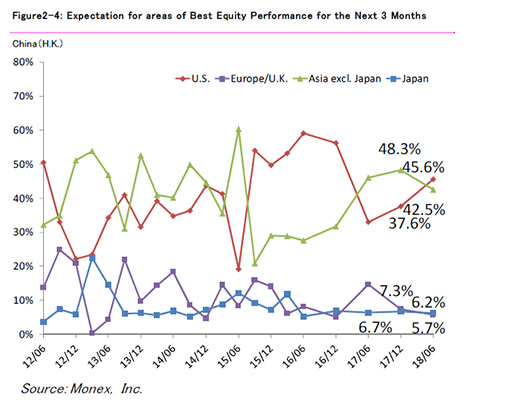

[China (H.K.)]

|

U.S.: 45.6%

|

Europe/U.K.: 5.7%

|

Asia excl. Japan: 42.5%

|

Japan: 6.2%

|

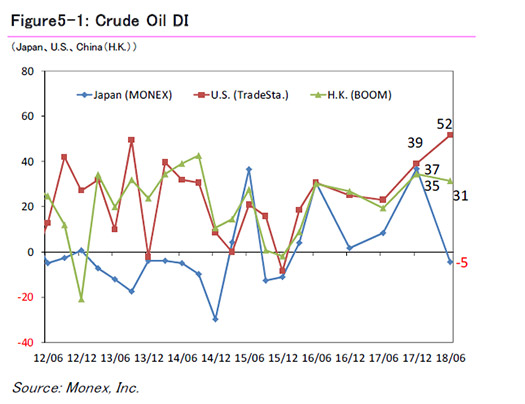

[Expectations for Crude Oil]

[Japan]

|

Dec. 2017: 37 → June 2018: -5 (-42 points)

|

[U.S.]

|

Dec. 2017: 39 → June 2018: 52 (+13 points)

|

[China (Hong Kong)]

|

Dec. 2017: 35 → June 2018: 31 (-4 points)

|

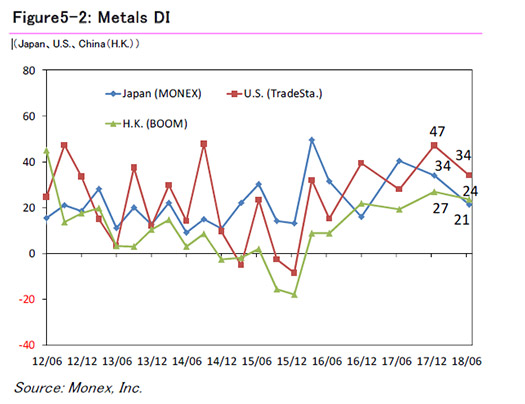

[Metals]

[Japan]

|

Dec. 2017: 34 → June 2018: 21 (-13 points)

|

[U.S.]

|

Dec. 2017: 47 → June 2018: 34 (-13 points)

|

[China (Hong Kong)]

|

Dec. 2017: 27 → June 2018: 24 (-3 points)

|

Results

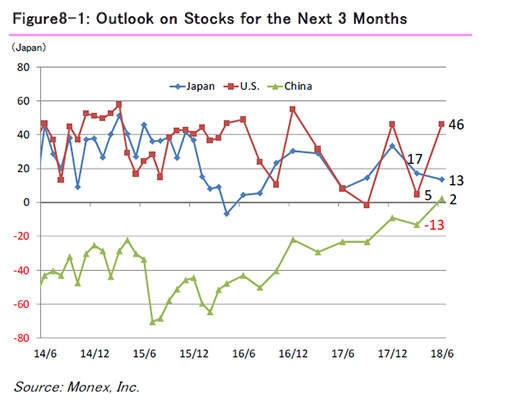

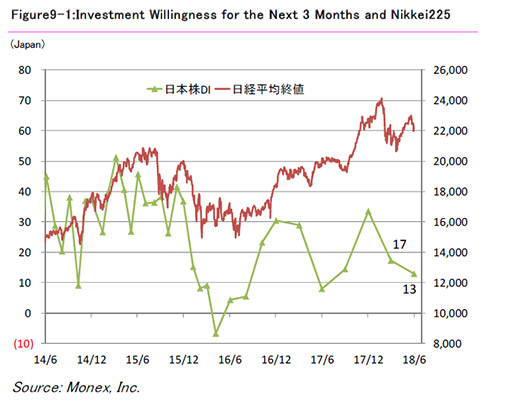

Results [Japanese Stocks DI]

|

March 2018: 17 → June 2018: 13 (-4 points)

|

[U.S. Stocks DI]

|

March 2018: 5 → June 2018: 46 (+41 points)

|

[China stocks DI]

|

March 2018: -13 → June 2018:2 (+15 points)

|

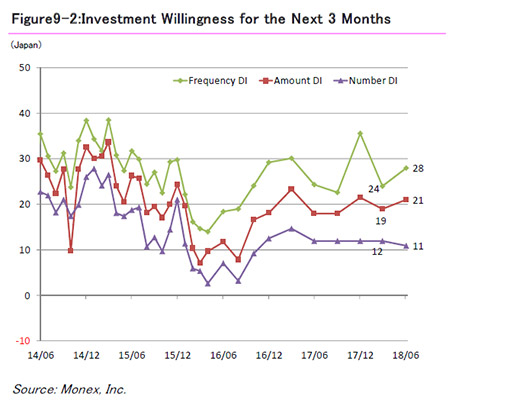

[DI of trading frequency]

|

March 2018: 24 → June2018: 28 (+4 points)

|

[DI of investment amount]

|

March 2018: 19 → June2018: 21 (+2 points)

|

[DI of the number of stocks held]

|

March 2018: 12 → June2018: 11 (-1 points)

|

Japan

Method:

|

Online survey

|

Respondents:

|

Customers of Monex, Inc.

|

# of Responses:

|

532

|

Period:

|

May 28 to June 4, 2018.

|

United States

Method:

|

Online survey

|

Respondents:

|

Customers of TradeStation Securities, Inc.

|

# of Responses:

|

120

|

Period:

|

May 29 to June 1, 2018.

|

Hong Kong

Method:

|

Online survey

|

Respondents:

|

Customers of Monex Boom Securities (H.K.) Limited

|

# of Responses:

|

353

|

Period:

|

May 29 to June 1, 2018.

|

Disclaimer

The Monex Global Retail Investor Survey measures customer sentiment based upon answers to specific questions received from a random sampling of customers of Monex, Inc., TradeStation Securities, and Monex Boom Securities (H.K.) Limited. Details of the methodology used to conduct the survey are available upon request. Accuracy and completeness of the data derived from the survey are not guaranteed.